1. Equity of the owner consists of business side debt to its owner.

2. Owner equity is shown by the following formulas:

| a) Equity + Liability = Owner’s Asset | Assets for business operations are provided by the owner’s funds (owner’s equity) and funds from external parties (liabilities) |

| b) Owner’s equity = Asset | – Owner claims on business assets are only made after the outsider’s claim is met first – Owner’s equity is a waste claim on a business asset after all liabilities are settled |

| c) Owner’s equity = Preliminary Capital + Additional Capital - Profit Loss – Takeout | Owner’s equity will increase if any: – Additional capital – Profit Loss (Revenue > Expenses) Owner’s equity will decrease if any: – Takeout – Profit Loss (Expenses > Revenue) |

3. The owner’s equity is recorded in Capital Account. Any increase in owner equity is credited in the Capital Account whilst any reduction in owner equity is debited in the Capital Account.

The Increase of Owner Equity

1. Owner equity will increase if:

a) there is additional capital by the owner

b) net profit is derived from profitable business operation

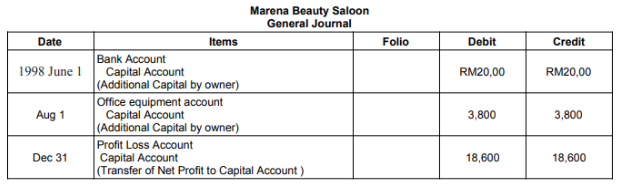

Example 1:

On January 1, 1998, the remaining capital of Marena Beauty salon was RM35000.

On 1 June 1998, he decided to expand his business by transferring cash of RM20000 from his personal bank account to business bank account. On August 1, 1998, Marena brought in a self-proprietary computer worth RM3800 into the business so that business accounting was managed more systematically.

For the year ended December 31 1998, Marena Beauty Salon Profit Loss Account recorded a net profit of RM18, 600.

Entry in General Journal

Journal entries for additional capital on 1 June and 1 August 1998, and net profit transfer to Capital Account on 31 December 1998 are shown in the following General journals.

Reduction of Owner Equity

1. Owner equity will decrease if :

a) there is a takeover by the owner

b) net loss is derived from unprofitable operations

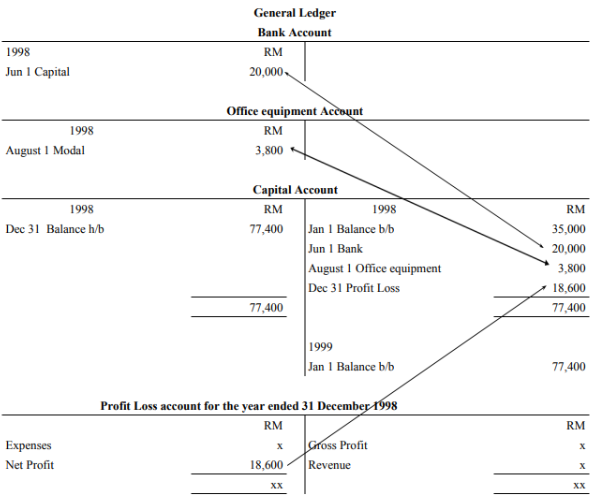

Entries in General Ledger and Profit Loss Account

2. As a summary, the double entries to record the addition of owner equity are:

a) Additional capital

Debit Asset Account

Credit Capital Account

b) Profit Loss transfer to Capital Account

Debit Profit Loss Account

Credit Capital Account